The Veterinary Hospital Income Statement

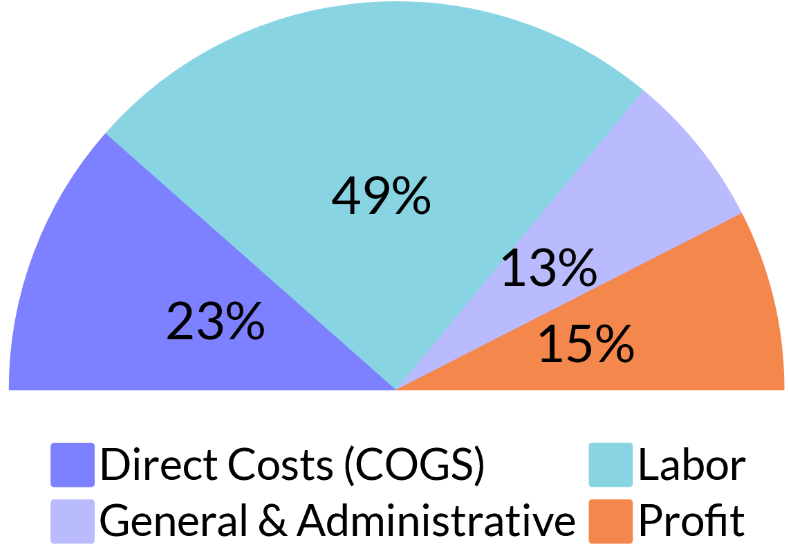

The big picture! A veterinary practice’s income statement (also referred to as the Profit/Loss Statement) can be divided into four broad categories: Direct Costs, Labor, General & Administrative, and, Profit.

Veterinarians are raised first as scientists (pre-veterinary study heavy on science), second as detectives (veterinary school study seeking out disease), and finally, if they become practice owners the entrepreneur in them is born.

For many, learning the business side of practice ownership is the result of trial and error, learning business from colleagues and consultants, attending CE, and, for many, ultimately running the practice much like the family checkbook. It is the latter approach that leads to practices resulting in no or low value when the time to sell rolls around.

Direct costs

Direct Costs (aka COGS – Cost of Goods Sold) are the costs paid to acquire the items (or services) needed to deliver products and services the to clients of a practice. Many practice income statements tend to record all these costs in one account labeled “Drugs & Supplies. Collecting all invoices from vendors and putting them in one account does not allow for the identification of cost centers where a practice owner or practice manager can identify opportunities to improve performance. When properly tracked on an income statement, direct costs have up to twelve parent accounts and twenty-five subaccounts. The level of granularity a practice follows determines their ability to manage total COGS.

Labor

Labor is an aggregation of all expenses tied to maintaining a thriving, productive workforce. Payroll (exempt & non-exempt team member, also referred to as salary and hourly) is the largest expense account in labor, however, the other accounts can impact overall labor costs significantly. The other accounts, commonly included on most practice’s income statements include payroll taxes, benefits and other employee expenses. Collectively, labor typically represents the greatest expense on a veterinary income statement.

General & Administrative

General & Administrative (G&A) is a large bucket of accounts on the income statement where bookkeepers allocate expenses associated with facility & equipment, administrative costs, advertising, income collection fees, depreciation, amortization, taxes paid on behalf of the entity or owners and miscellaneous expenses.

Profit

Profit represents the net income at the bottom of the income statement. Profit does not represent the overall true value of practice ownership as there are legitimate expenses tied to practice ownership under G&A that are “added back” to the profit figure. These expenses do not carry over to the new owner in a practice sale. When these expense accounts are added to the profit, a new value is created called EBITDA. VizVet calculates the practices EBITDA as that represents to true monetary benefit of practice ownership. To better understand EBITDA, refer to this article.